2017 was a year of large investments in Startups

For anyone who had been following the news around startups in the UK along the past year, the year of 2017 has been a record year in terms of investment into new and innovative companies.

Several industry sectors benefited from this trend. Fintech, for instance, has been growing exponentially and shows no signs of slowing. There is also apparently more interest from government in the high-growth ecosystem than perhaps any time in history. But other sectors are rose in 2017, like Artifical Intelligence or the subscription based model.

If you are interested in a great analysis on the investments made on startups for 2017, check the research report by Beauhurst.

2017 UK Startups overview

The growth of Fintech

Business Insider has been highlighting since 2016 that Fintech could be bigger than ATMs, PayPal, and Bitcoin combined. Even though 2017 was one roller-coaster year for Bitcoin, it was a great year for all Fintech businesses in the UK. In 2017, the country’s Fintech sector attracted around £1.3 billion of funding, according to both PitchBook & Beahurst.

Breaking the classic banking business models, Fintech startups have been using technology to help people and businesses manage their finances, make transactions or investments. There is still some concern from investors regarding how B2C Fintech companies will actually make money as their business model is often quite different from standard retail or investment banking.

Some startups which raised funding in early 2017 have already become a household name, such as Transferwise, with $280m raised from a set of investment heavyweights. These startups are now competing with established brands and pushing for innovation.

A new successful business model: subscription

The subscription business model has been blooming in 2017 – as well as their ads on the Tube. Previously only seen in newspapers, magazines, gyms, utilities, and telecommunications firms, more products and services are being offered to more people through subscriptions than ever before.

In essence, this business model is quite straight-foward: customers can receive any product – whether it be food, clothing, or cosmetics – delivered as often as suits them. Although the idea can be tricky to pitch as it is hard to value the company with classic top-down finance models, a bottom-up valuation starting from an analysis of the different types of customers enables to get a great idea of the potential for a new business (see Harvard Business review).

The investors have well understood this and dropped a record amount of funding: in 2017 they raised a total of £18.4 million, over 16 rounds of fundraising.

Artifical Intelligence

Gartner AI & Machine Learning Magic Quadrant 2018

This trend is a great deal for both large and small companies. The interesting bit is that although large companies have a great amount of data they can leverage of AI (artificial intelligence) and machine learning, they don’t always have the flexibility needed to kick-start this kind of ground-breaking Big Data projects. On the other hand, startups have proven that they can attract hard-to-catch Data Scientists with interesting concepts and ideas and create AI-based business models. It is also interesting to see that looking at the Gartner Quadrant for AI for 2018, several companies are less than 5 years old, like Domino or Dataiku. And these companies are already competing or partnering with established brands in the industry, like Teradata, SAP, SAS or IBM.

AI companies raised a record £488 million last year, according to data compiled by funding database PitchBook for London & Partners. That’s more than twice what was raised in 2016.

The UK has also gained a global reputation for AI thanks in part to four of the biggest AI startup acquisitions of the last five years. That began when Google swept up DeepMind in 2014 for a reported £400 million. Then there was Apple’s purchase of natural language processing (NLP) specialists VocalIQ, Microsoft’s purchase of machine learning-powered keyboard SwiftKey, and Twitter’s acquisition of Entrepreneur First alumni Magic Pony.

Business models and sectors applications for AI are broad and as the technology becomes more accessible, 2018 should see reality replaces hype through deep learning, data governance, conversational AI.

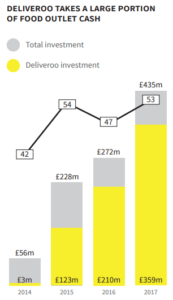

Food delivery

Beauhurst research The Deal 2017

Growing on a similar trend as the subscription box model, food delivery business have been flourishing in the UK in 2017. Across the year an enormous £435m was injected into various food outlet businesses across 53 announced fundraisings. This figure is almost double the investment raised in 2015. However, looking at the funds each investor gave, all of them went to the online takeaway service Deliveroo.

But a lot of other players can also be found from traditional restaurants, cafes and bakeries, farming, food collection and health-based business models. The latest reflecting the increasingly health-conscious society we are living in, and the recent rise of veganism in the UK.

2018 upcoming trends

As 2017 was a great year for startups, although 2018 will continue to cope with Brexit, it is sure to also be a great year for some other sectors in the startup landscape. Here is our top pick at Rising Digits:

Esport

This is another topic that has been increasingly mentioned by the Business Insider this year and will continue next year. The eSports competitive video gaming market continues to grow revenues & attract investors, 2018 will become one of the best years of Esport with already 28 great tournaments scheduled in the UK.

Western Europe is the second-largest region in terms of revenues with $169 million in 2018 according to Newzoo. Western Europe, more than any other region, is characterized by localized esports ecosystems that operate next to regional tournaments and leagues. Some notable examples are ESWC (France), Gfinity (UK), and LVP (Spain). As audiences across countries are culturally diverse, many sponsors, media companies, and investors that operate on a local level are looking for esports initiatives that match their strategy. Sponsorship will remain the biggest revenue stream with $62.9 million, while media rights will total $26.6 million this year, a year-on-year growth of 49% still according to Newzoo.

The UK Esport market will see a 27.6% compound annual growth rate (CAGR), reaching £8m in consumer ticket sales only by 2021 while Digital advertising in Esports will increase by 46.2% CAGR to £12m by 2021 according to PWC.

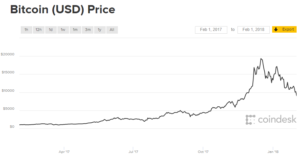

Cryptocurrencies & Blockchain

Coindesk Bitcoin Price 2017

As mentioned previously, 2017 was a roller-coaster year for crypto-currencies, seeing Bitcoin rise and plummet.

Yet, 2017 was also a ground-breaking year for Bitcoin and other cypto-currencies as some countries like Japan have declared the currency legal and bitcoin futures approved by the CFTC at the end of 2017.

Globally, the cypto-currencies sector can be broken down into 4 pillars: exchanges, wallets, payments and mining. For the UK market, already strong in the financing sector, the first 3 are booming and see a lot of new startups.

- The UK is the 1st market for crypto Exchanges, representing 18% of the global number based on a study by the Cambridge University.

- The Uk is the 2nd market for wallets, with 15% of shares, based on the same report.

- It is also second in terms of payments, with 15% too.

- Mining on the other hand is mainly focused between China and the US.

Additionally, 2017 was also an impressive year in terms of a new funding method: Initial Coin Offerings (ICOs). CoinDesk’s ICO tracker logged over $3.5 billion in funds raised via ICOs! This new method of investment should still pursue in 2018 even though some regulations are bound to happen in 2018 too.

As always, if you are working on one of these interesting sectors and need some support regarding your business model, niche market research or just web-services, feel free to reach to me and let’s discuss!